How Relevant are the Maastricht Criteria in the Current Economic Environment?

How Relevant are the Maastricht Criteria in the Current Economic Environment?

Pavel Patakov // 22 January 2025

According to the Treaty on the Functioning of the European Union, adopting the euro as the national currency is a mandatory requirement unless an explicit exception is agreed upon. How relevant and applicable are the so-called Maastricht criteria – the conditions that each country must meet to become part of the eurozone – today?

The Maastricht criteria are five in number and aim to assess the degree of economic convergence. They include requirements for:

- Inflation – According to the harmonised consumer price index (HICP), inflation should not exceed 1.5% above the average value of the three EU countries with the lowest inflation.

- Budget deficit – The country must not be in an excessive deficit procedure, which typically (but not always) means the deficit should be below 3% of GDP.

- Government debt – the debt-to-GDP ratio must be below 60%, and if it exceeds this threshold, there should be a trend of sustainable reduction.

- Long-term interest rates – Similar to the inflation requirement, the key benchmark is again the three EU countries with the lowest inflation, and the allowed excess is 2%.

- Exchange rate stability – The requirement aims to ensure the stability of the national currency against the euro, meaning the currency must have been in the ERM2 exchange rate mechanism for at least two years.

How relevant are these criteria in the current economic and political landscape in Europe?

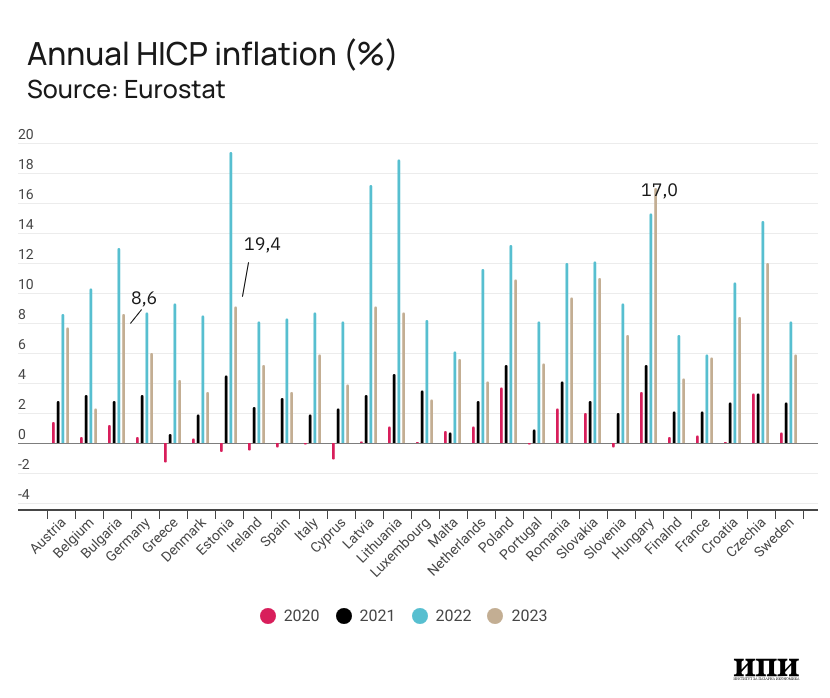

In 2022, almost all EU countries saw a significant increase in inflation. This was primarily due to global market factors and the economic consequences of the war in Ukraine, which led to sharp disruptions in energy supplies, and secondarily, to other key raw materials and food.

The highest inflation in 2022 was observed in the Baltic states – Latvia (17.2%), Lithuania (18.9%), and Estonia (19.4%), as well as in Hungary (15.3%) and the Czech Republic (14.8%). These countries faced greater difficulties due to their dependency on Russian gas and their more limited capacity to quickly adapt to new energy sources.

In 2023, inflation started to decrease in most countries, including Bulgaria, where the inflation (annual average) fell from 13.0% in 2022 to 8.6% in 2023. This was the result of stabilisation in the energy markets and efforts by central banks in the EU to control inflationary pressure by raising interest rates.

However, in Hungary, inflation remains extremely high (17.0% in 2023), which is an anomaly compared to trends in the rest of Europe. This is explained by the ongoing energy crisis in the country and the continuously weakening national currency, which further pressures prices.

While most European countries are gradually bringing inflation under control, it remains important to monitor and strengthen measures for energy independence and financial sustainability to avoid another price spike in the event of future disruptions in global markets.

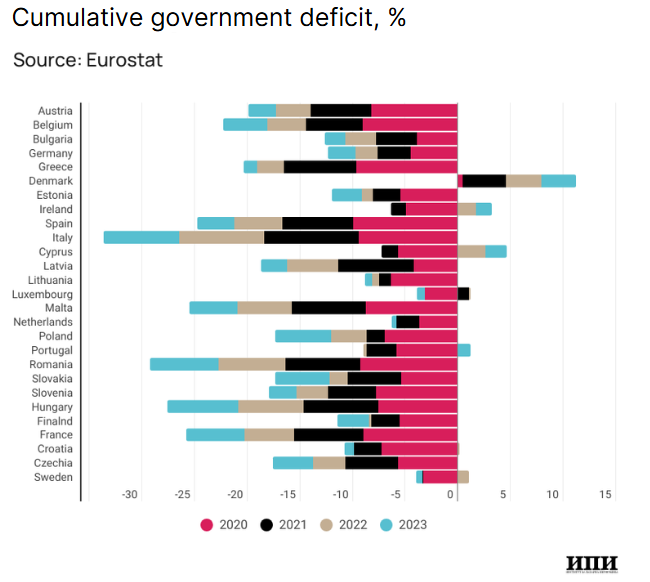

The pandemic, which began in 2020, caused significant fiscal challenges for EU countries, as governments were forced to increase healthcare spending, subsidise affected businesses, and implement broader social measures to support vulnerable groups. Data shows that deficits reached unprecedented levels in almost all member states. Only Denmark managed to maintain a positive budget balance (+0.4%), while all others exceeded the 3% threshold. The most affected countries – Spain (-9.9%), Greece (-9.6%), and Italy (-9.4%) – already had structural economic weaknesses from the previous debt crisis, highlighting their vulnerability during economic shocks.

However, in 2021 and 2022, as economies gradually recovered and most restrictive measures were lifted, a trend of improvement in the budget balance was observed. Deficits began to shrink, as countries reduced spending on crisis measures and focused on structural reforms and investments. It is important to note that in 2022, some countries like Ireland (+1.7%), the Netherlands (+0.0%), and Portugal (-0.3%) managed to stabilise their budgets to the point of reporting minimal deficits or even surpluses. These positive results reflect both a quicker return to growth and the start of national recovery and resilience plans (NRRPs), supported by EU funds.

In 2023, however, a new increase in budget deficits occurred in many countries, linked to new economic challenges arising from the war in Ukraine. The conflict led to higher defence spending, increased subsidies to offset energy costs, and additional spending to support households and businesses. Countries like France (-5.5%), Hungary (-6.7%), and Romania (-6.5%) continue to face significant deficits, indicating the difficulties in managing new crises.

Bulgaria remains one of the countries with the lowest debt-to-GDP ratio in the European Union, with debt at just 22.9% in 2023. This persistently low value reflects the long-standing conservative fiscal policy followed. Low debt levels in Bulgaria and other countries with low debt, such as Estonia (20.2%) and Luxembourg (25.5%), provide financial flexibility and stability during economic crises, allowing for investment and more sustainable budget management.

At the same time, the economies of Greece and Italy face significant difficulties in reducing their debt. In 2023, Greece’s debt stands at 163.9% of GDP, while Italy’s is 134.8%, despite both countries having reduced their debt levels from the peaks in 2020.

In 2023, only about half of EU countries manage to meet the criterion of debt below 60% of GDP. This divides the Union into two clearly distinguishable groups: countries with low debt levels (Bulgaria, Estonia, Luxembourg, Czech Republic, and Sweden) and those with high debt exceeding the Maastricht criteria (Greece, Italy, Portugal, France, Spain, and Belgium). This situation creates different economic realities in individual countries, with high-debt countries facing stricter fiscal discipline and reforms imposed by the EU, while those with low debt maintain more freedom in managing their public finances.

After the pandemic, many European countries have begun significantly reducing their debt levels, and the trend of shrinking debt is visible in the data for the period 2020-2023. This change is due to the stabilisation of economic activity, increased tax revenues, and the efforts of many governments to limit budget deficits in order to achieve greater fiscal sustainability.

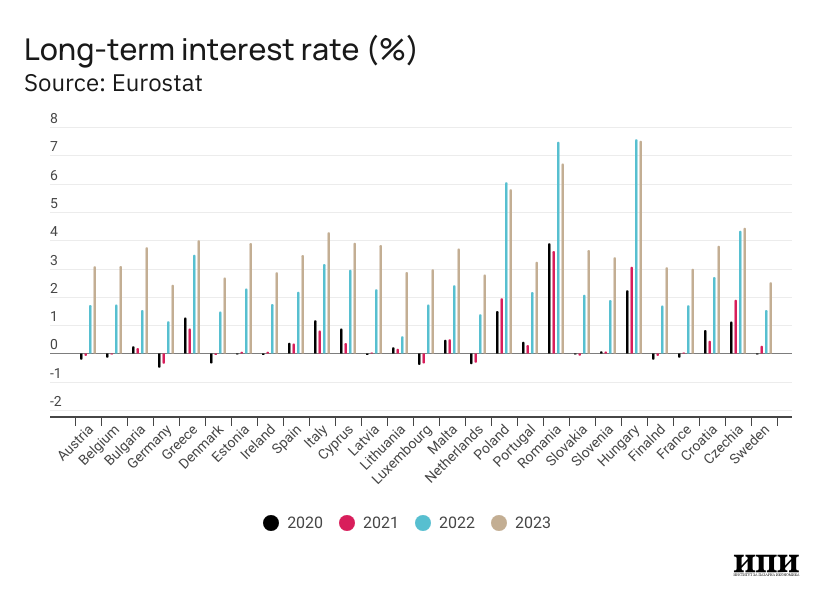

In recent years, interest rates on long-term government bonds in the EU have risen significantly, after being at historically low levels in 2020. For Bulgaria, the rates started at 0.25% in 2020 and rose to 3.75% in 2023, following the general trend in the Union, but with a slower increase than in some other countries like Romania and Hungary.

Interest rates are rising in response to high inflation, which accelerated in the second half of 2021 and reached record levels in 2022. The European Central Bank tightens its monetary policy, which includes both raising interest rates and limiting liquidity. This increases financing costs for governments, including Bulgaria, and signals broader global economic challenges. Despite this rise, interest rates on deposits and some loans in Bulgaria remain lower compared to countries with higher debt, indicating stability in our public finances.

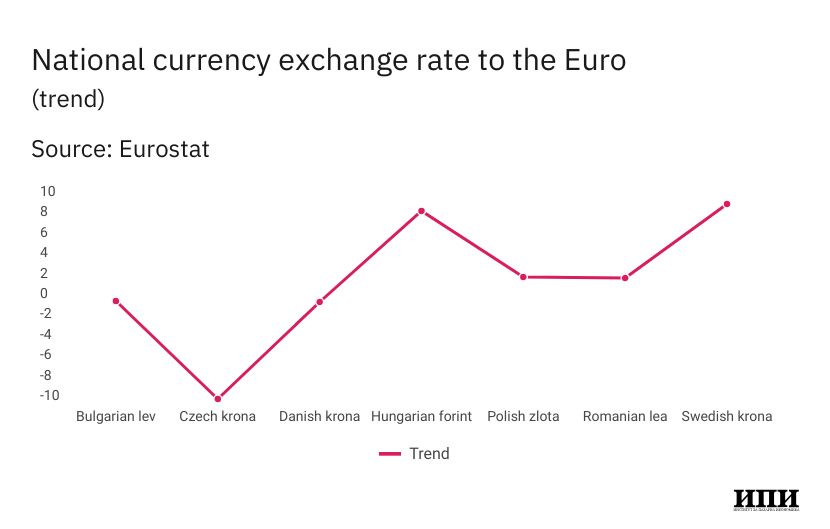

For countries outside the eurozone, the stability of the exchange rate against the euro remains of essential importance. Trends in countries outside the eurozone – except for Bulgaria, which has a fixed exchange rate through the currency board, and Denmark – are diverse. In Poland and Romania, there is relative stability in exchange rates, which is the result of successful macroeconomic policies, while in Sweden and Hungary, there is a significant depreciation of their national currencies. These differences highlight the importance of currency stability and the impact of domestic economic policies on national currencies’ exchange rates against the euro.

|

|

Inflation, % |

Deficit, % of GDP |

Debt, % of GDP |

Long-term interest rate |

Lev/Euro exchange rate |

|

2020 |

1.2% |

3.8% |

24.4% |

0.25% |

1,9558 |

|

2021 |

2.8% |

3.9% |

23.8% |

0.19% |

1,9558 |

|

2022 |

13% |

2.9% |

22.5% |

1.53% |

1,9558 |

|

2023 |

8.6% |

2% |

22.9% |

3.75% |

1,9558 |

The Maastricht convergence criteria are proving to be an increasing challenge for many EU economies. Practically, countries within the eurozone that do not breach the budget deficit and public debt thresholds are already exceptions. This underscores the need for a debate on the overall framework based on criteria conceived more than three decades ago.

This blog was originally published in Bulgarian by the IME.

EPICENTER publications and contributions from our member think tanks are designed to promote the discussion of economic issues and the role of markets in solving economic and social problems. As with all EPICENTER publications, the views expressed here are those of the author and not EPICENTER or its member think tanks (which have no corporate view).

{kind=link}

{kind=link}

{kind=link}

{kind=link}