How Much Do European Countries Spend on Defence, and How Much Does It Matter to Them?

How Much Do European Countries Spend on Defence, and How Much Does It Matter to Them?

Adrian Nikolov // 9 April 2025

Amid the heated transatlantic disputes of the last few weeks and the realisation that the US wants to play a smaller role in the defence of Europe, one thing is becoming clearer – the EU in the coming years will have to invest more in defence. This is likely to be at the expense of other areas, including infrastructure and agriculture. Our aim here is not so much to look at potential future changes as to present the current state of military spending, its distribution, as well as the state of the military-industrial complex.

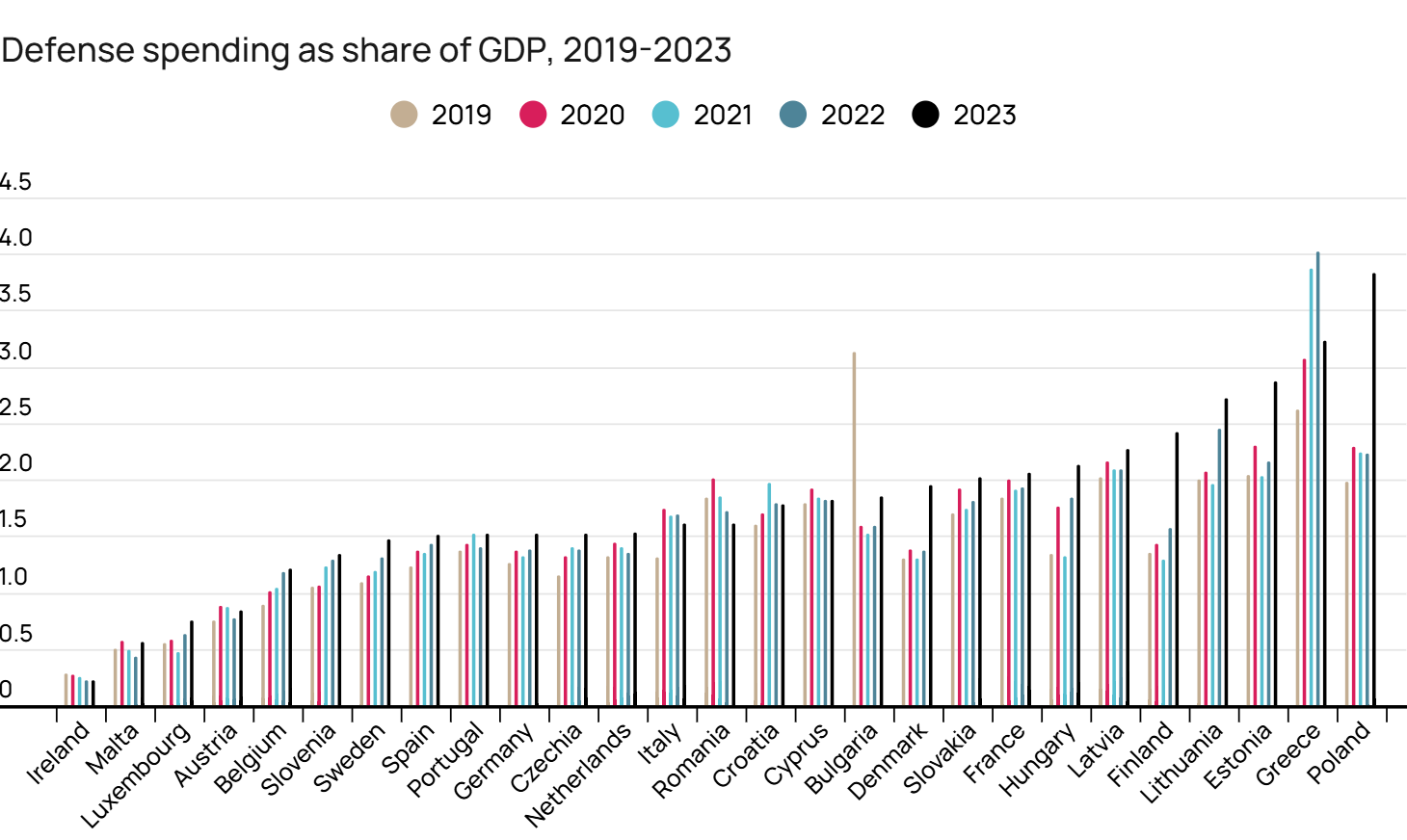

The importance of defence in national politics is most clearly seen in the share of GDP that the state spends on military. The latest available data (for 2023, from the Swedish Institute for Peace Research, SIPRI) shows very large differences in the focus on defence of different European countries. Even leaving aside Ireland, whose GDP has a particular structure because of the digital giants, there are European countries where defence is not a particular priority – even after the start of the war in Ukraine, for example, Austria spends only 0.84% of GDP, Belgium 1.21%, Slovenia 1.34%. The countries with the highest share of military spending are Poland (3.83%), Greece (3.23%), Estonia (2.87%), Lithuania (2.72%), Finland (2.42%). As expected, most countries with a high share of military spending in 2023 border with the military conflict.

As expected, the war leads to an overall increase in the share of military spending; this is most visible in Poland, where the increase is in the order of 1.6 percentage points of GDP compared to 2022, and in Finland and Estonia, where the increase is 0.85 and 0.71 percentage points, respectively. In most countries, including Bulgaria, the increase is in the order of 0.1-0.3 percentage points. It is important to note that some large purchases of military equipment can lead to large one-off deviations – for example, Bulgaria in 2019 spent 3.1% of GDP due to the purchase of F-16 aircraft, although its usual defence spending is in the order of 1.6% of GDP.

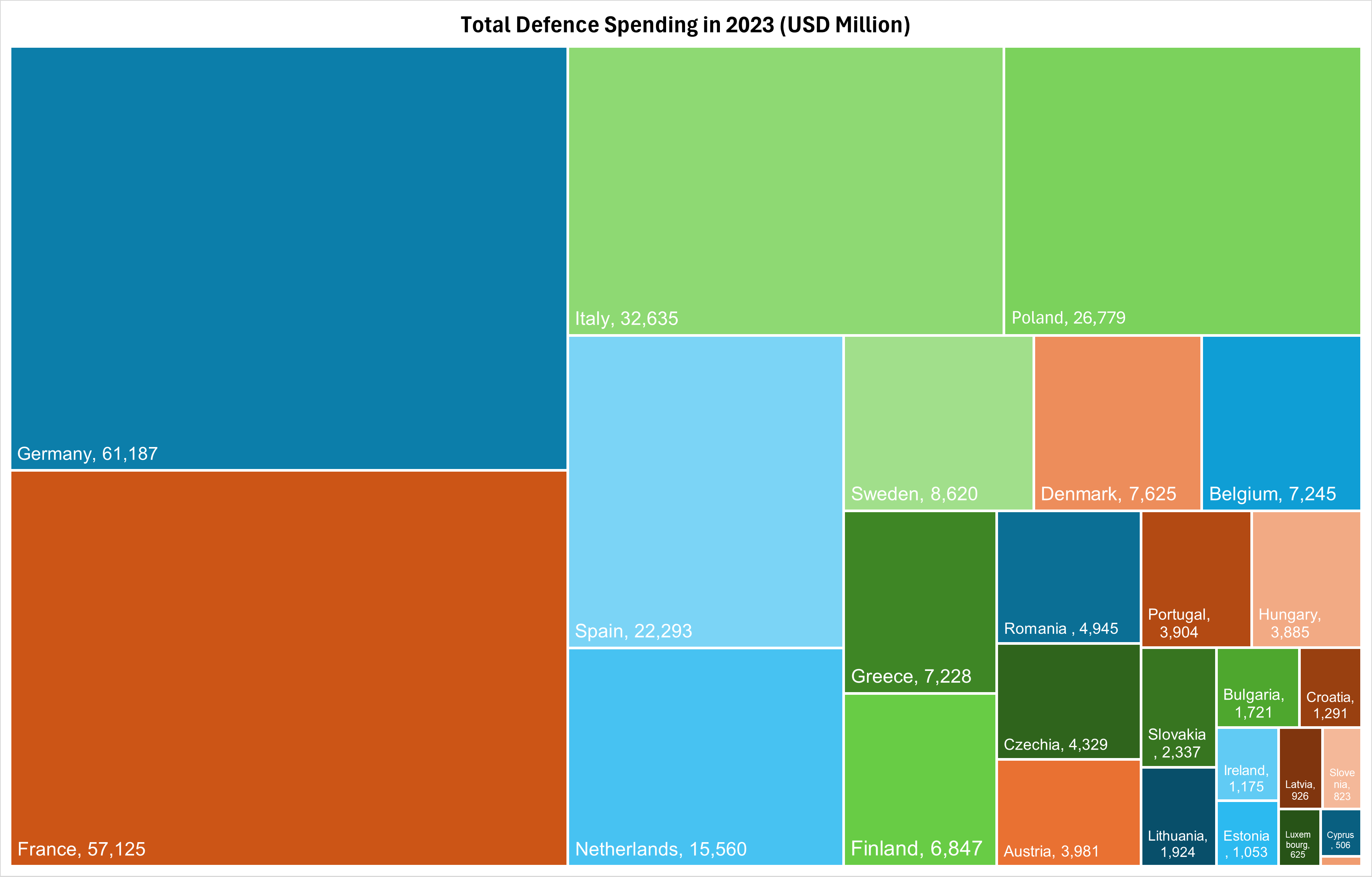

In military expenditure, the nominal size matters no less than the relative size. Here the major European economies lead the way – according to SIPRI data, Germany is the absolute leader with $61 billion USD, followed by France with $57 billion USD, Italy ($33 billion USD), Poland ($27 billion USD) and Spain ($22 billion USD). For comparison, the amount of German spending almost equals the amount of the 20 Member States at the bottom of the table. Summing up the spending of all European countries, the total amounts to $287 billion USD in 2023. This puts in perspective the proposed new investment in the order of €800 billion, which would be equivalent to the EU's total military spending for almost three years so far.

In a dynamic, the Russian invasion of Ukraine has led to an 11% increase in defence spending in the EU as a whole in 2023. However, the growth is highly uneven between member states, with Poland increasing its spending by 75%, Finland by 54%, and Denmark by 39%. In this context, the increases in the major European economies are more modest, with Germany's spending rising by 9%, France's by 6%, and even Italy's shrinking by 6%.

The proposed sharp increase in military spending is also seen as a stimulus to European industry, especially because of the inevitable need to redirect other spending in that direction. According to SIPRI data on the world's largest arms manufacturers, there is not a single European company in the top 10 in terms of global sales revenue, with only Airbus, Italy's Leonardo and France's Thales in the top 20, and Rheinmetal and MBDA in the top 30. This in no way means that Europe does not have the potential for arms production, or that the capabilities of smaller manufacturers (including Bulgarian ones) should be ignored. It should be clear, however, that if among the objectives of military spending is to be the revitalisation of domestic industry, not only more intensive purchases but also a major expansion of production capacity as well as development will be needed in the medium term.

In any case, we are facing a paradigm shift, and in the coming years we will hear more and more about defence investment and spending. As we have clearly demonstrated, today this sector is far from being an equally high priority for all member states, and because of the great disparities in the size of European economies, the larger ones can afford far more armaments. The transition to a common European defence policy will change this distribution, and the EU seems to be moving towards a defence priority similar to those set today by the countries on its eastern border.

Adrian Nikolov is a Senior Economist at the Institute for Market Economics in Bulgaria.

This blog was originally published by the Institute for Market Economics in English and Bulgarian.

EPICENTER publications and contributions from our member think tanks are designed to promote the discussion of economic issues and the role of markets in solving economic and social problems. As with all EPICENTER publications, the views expressed here are those of the author and not EPICENTER or its member think tanks (which have no corporate view).

{kind=link}

{kind=link}

{kind=link}

{kind=link}